Mortgage rates decreased for the third straight week, according to the Freddie Mac (OTCQB: FMCC) Primary Mortgage Market Surveyâ

Sam Khater, Freddie Mac’s chief economist, said rates were at their lowest level since mid-April. “Backed by very strong consumer spending, the economy is red-hot this month, which is in turn rippling through the financial markets and driving equities higher,” he said. “Unfortunately, the same cannot be said about the housing market, where it appears sales activity crested in late 2017. Existing-home sales have now stepped back annually for the fifth straight month, and purchase mortgage applications this week were barely above year ago levels.”

Added Khater, “It is clear affordability constraints have cooled the housing market, especially in expensive coastal markets. Many metro areas desperately need more new and existing affordable inventory to break out of this slump.”

News Facts

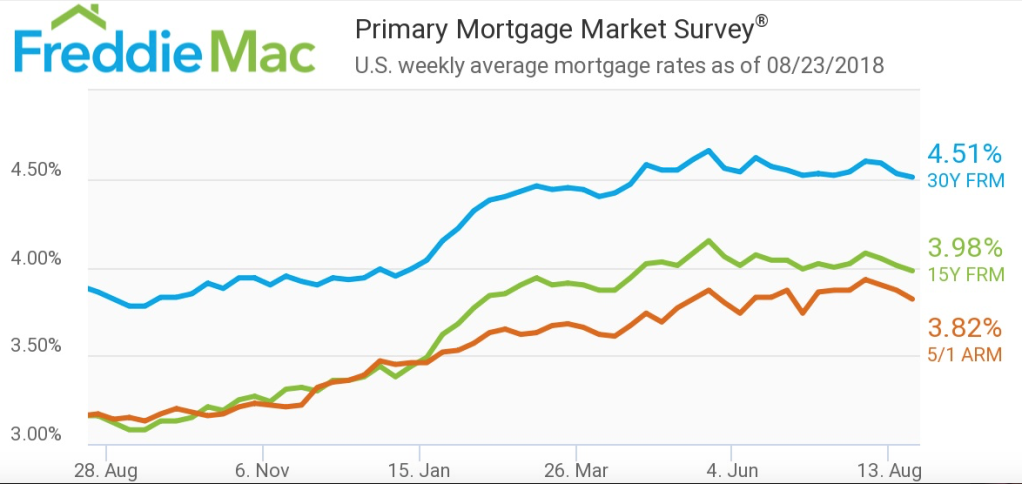

· 30-year fixed-rate mortgage (FRM) averaged 4.51% with an average 0.5 point for the week ending August 23, 2018, down from last week when it averaged 4.53%. A year ago at this time, the 30-year FRM averaged 3.86%.

· 15-year FRM this week averaged 3.98% with an average 0.5 point, down from last week when it averaged 4.01%. A year ago at this time, the 15-year FRM averaged 3.16%.

· 5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.82% with an average 0.3 point, down from last week when it with an average 3.87%. A year ago at this time, the 5-year ARM averaged 3.17%.

Brian Surgener, SVP Strategy & Analytics at BBMC Mortgage, said, “It’s pretty much the same story it has been. We need to see wage growth or a way to market the American Dream for the millennials. It is great to see mortgage rates hold around 4.5%. They are still historically low but we are not seeing the traction we have hoped to see in purchase applications. Though more people are employed today than they were last year we are not seeing them move up in home size or out of their rentals and into a new home. Instead they are spending money on gadgets or updating their current homes.”