The question I am always asked in seminars I give around the country is, “What markup should I use?” I always give the same, simple answer, “It depends.” Each custom builder must evaluate his or her own situation in order to establish the markup percentage that will cover operating expenses and provide a reasonable profit.

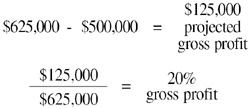

Many custom builders confuse the term markup with gross profit (sometimes referred to as margin or gross margin). Markup is simply the factor that you apply to your estimated job costs to determine sales price. For example: You estimate the cost of the Jones house to be $500,000. Using a markup of 25%, you determine the selling price should be $625,000 ($500,000 x 1.25 = $625,000).

Gross profit, on the other hand, is computed by subtracting cost of sales (sticks and bricks) from your contract price. The gross profit percent is equal to gross profit divided by the contract price. In the above example the targeted gross profit would be 20%, computed as follows: Make sure that you understand the difference between markup and gross profit. If you know your targeted markup percent and want to determine the targeted gross profit percent, divide the markup percent by 1 plus the markup percent. For example: You are marking up 50% and want to know what gross profit that markup would achieve.

In order to avoid confusing markup and margin you may want to use the following method for pricing your jobs. Instead of marking up your costs using a markup, divide your costs by 1 minus your targeted gross profit. Using this method you would price the Jones house as follows:

Another way of pricing a new home is to apply a markup to your estimated costs. Following is a step-by-step guide for identifying your target markup:

- Establish a target profit. The first step is to determine how much profit you would like to make. This amount should be after paying yourself a “reasonable” salary for the work that you perform for the company. Suppose you anticipate building (and selling) five houses this year at an average sale price of $600,000. Your anticipated sales volume would be $3 million. Now suppose you would like to make a net profit of $250,000 this year. This return is in addition to your annual salary, which is included in operating expenses.

- Identify overhead expenses. Go through your chart of accounts and establish a budget for each of your detailed operating expense items. Overhead includes things like salaries (yours as well as those of employees), office rent, office supplies, phones, vehicles, etc. For this example, we’ll suppose that your annual budget is $500,000.

- Compute projected gross profit. Your gross profit must cover your entire overhead and your net profit. In our example, to cover overhead and provide projected net profit, you will need a gross profit of $750,000 ($250,000 net profit plus $500,000 in overhead expenses). This equates to a targeted gross profit of 25% ($750,000/$3,000,000 = .25)

- Calculate markup. In order to determine the markup you need, first compute your targeted cost of sales by subtracting your targeted gross profit from your total revenue estimate ($3,000,000 sales volume – $750,000 targeted gross profit = $2,250,000 targeted cost of sales). To determine your target markup, divide sales by cost of sales. In this example our targeted markup would be 1.33 ($3,000,000/$2,250,000 = 1.33).

As you can see, markup is different than gross profit. If we were to use a 25 percent markup instead of a 25 percent gross profit (1.33 markup), we would only achieve a gross profit of $600,000, not $750,000 (20 percent x $3,000,000 = $600,000). That would reduce our projected net income from $250,000 to only $100,000 ($600,000 gross profit -$500,000 of overhead = $100,000). Another method of pricing new homes would be to use market-based pricing. This works especially well for pricing a spec home.

When pricing a spec home I suggest using a top-down approach. Start with your sales price and then subtract the amount of profit you want to make. The number that is left should be how much you can spend to build the house. For example, let’s assume that you envision the house you want to build will sell for $500,000. For your risk, you target a 25% gross profit ($125,000). The lot will cost you $75,000 and you will have to pay a 5% commission ($25,000) to an outside real estate agent. Assuming you will be taking a loan to finance construction, you anticipate interest expense (including carrying the house for three months) to be $35,000. Now develop your construction estimate. If it shows that you are not able to build the house for $240,000 ($500,000 sales price – $125,000 profit – $75,000 for land -$25,000 commission – $35,000 financing expense = $240,000), it is time to go back to the drawing board and decide what features you can pull out of the house to get hard costs down to $240,000.

When I discuss their financial results with new Builder 20 Club groups, I ask each member to identify the markup he or she typically uses to price a house. In the most recent meeting I attended, the markup ranged from multiplying by 1.135 to dividing by .72, which resulted in the sales price on a home with $1 million in direct construction costs ranging between $1,135,000 and $1,388,000. This diversity in markups and the method in which markup is applied is typical of all of the groups I visit. The builders with the low markups always say that their market is different and that they can’t get higher markups. I strongly believe the “not in my market” excuse is a cop-out. Looking at financial results of custom builders throughout the country, I see builders getting 1.2 and 1.25 markups in the same market as those builders saying they can only get 1.135. There are only two ways to get margin in the custom building business. The first is to sell it and the second is to keep it. The biggest problem that I have found is that many custom builders are afraid to ask for margin.

The following chart may assist you in comparing margin vs. markup:

30% Gross Profit = 1.430 Markup

25% Gross Profit = 1.330 Markup

20% Gross Profit = 1.250 Markup

18% Gross Profit = 1.220 Markup

16% Gross Profit = 1.191 Markup

14% Gross Profit = 1.164 Markup

Steve Maltzman, CPA, is president of SMA Consulting in Colton, Calif. Visit him at www.smaconsulting.net.