Having doubled in the past three years, the average lot supply among the top 10 builders relative to forecasted home sale trends is 5.8 years, close to an all-time high. This represents more than 2 million lots, which are in various stages of the entitlement and development process. The market share of these top 10 builders surged from 7 percent in 1990 to 23 percent today. In the same period, margins and returns doubled. We expect market share gains to continue for the next five years. By 2010, we believe 10 builders will control 50 percent of the single-family U.S. housing market. On the other hand, we believe margins and returns are likely to plateau in the next two years.

While above-average home price appreciation lifts margins, slow demand and lengthy entitlement periods negatively affect asset turns. So, builders incur higher carrying costs on their land. In light of this enormous lot supply and the higher costs of holding land, combined with slowing demand and near peak margins, capital expenditures on land purchase will likely ease in the next two years. In 2005, on average, leading builders allocated 90 percent of their capital to buy land. However, this slowed in the third quarter, as Centex and Pulte held their lot positions flat. In total, the top 10 builders spent some $20 billion on land in 2005. As they curb their land purchase consumption, prices should moderate and their dollars should go further. This, in turn, will free up capital for share repurchasing.

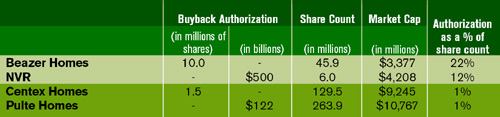

Since early November, 10 builders have announced share buyback programs for an average of 8 percent of their share counts. Among this group, Beazer Homes’ recent authorization of 10 million shares was the largest, representing some 22 percent of its total outstanding shares. The bears may argue that this is indicative of the slowing demand environment. But we believe the move stems more from depressed valuations than it does from a market turn. Smart builders know they can grow through a slowdown, and that they’ll come out stronger at the other end. As such, we believe focusing on buybacks at this moment is the best use of capital. Repurchases send a message of management’s confidence in their business models, rather than a desire to meet short-term goals or to go private.

We support accelerating repurchases as a way to return capital to shareholders. Let’s see how—and count the benefits.

Margaret Whelan is an analyst with UBS Investment Bank.

BUYBACK TICKER Share buyback plans differ widely among publics. Beazer and NVR are aggressively committing capital to share repurchases, while Centex and Pulte are not budging on ongoing opportunism in the land game.