Lennar Corp. (NYSE: LEN, LENB on Monday morning reported net earnings of $313.5 million, or $1.34 per diluted share for the fiscal fourth quarter ended Nov. 30, compared to net earnings of $281.6 million, or $1.21 per diluted share in the prior-year quarter. Analysts polled by The Wall Street Journal were expected earnings of $1.28 per share.

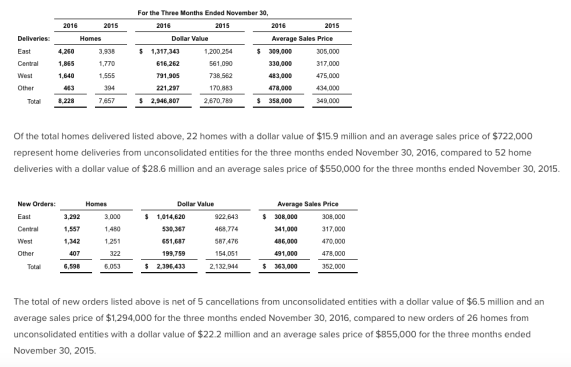

Revenue was up 15% to $3.4 billion on a 7% rise in deliveries to 8,228 homes. New orders rose 9% to 6,598 homes and the dollar value of orders rose 12% to $2.4 billion. Backlog jumped 15% in units to 7,623 and 17% in dollar value to $2.9 billion.

Gross margin on home sales was 23.3%, down from 24.6% in Q4 2015 but up 70 basis points from Q3 2016. SG&A expenses as a percentage of revenues from home sales improved to 8.7% from 9.2% in Q4 2015 and rose sequentially 60 basis points from Q3 2016.

Among operating segments, Lennar Financial Services posted operating earnings of $51.4 million, compared to $33.8 million in the prior-year quarter. Rialto operating earnings, net of noncontrolling interests, were $8.0 million, up from $7.6 million. Lennar Multifamily reported operating earnings of $41.4 million, compared to $10.2 million a year earlier.

Lennar ended the quarter with home building cash and cash equivalents of $1.1 billion, and no outstanding borrowings under its $1.8 billion credit facility. Debt to total capital, net of cash and cash equivalents, was 33.4%, compared to 42.2% in Q4 2015.

For the full fiscal year, the company reported net earnings of $911.8 million, or $3.93 per diluted share, compared to net earnings of $802.9 million, or $3.46 per diluted share in fiscal 2015, on deliveries of 26,563 homes, up 9%, new orders of 27,372 homes, up 9%, and revenues of $10.9 billion, up 16%.

“We have consistently believed that the housing market is continuing its slow and steady recovery, and we have crafted our operating strategies specifically to position our company to grow at a measured pace and to act opportunistically in these market conditions,” said Stuart Miller, Lennar CEO. “With the anticipation of a new President focusing on accelerating economic growth, we believe that our fortified balance sheet, our diversified business model and our refined product offerings, will continue to hold us in good stead in a high-growth economy, despite the potential of moderately rising interest rates over the next several years.”

On September 22, 2016, the Company entered into an Agreement and Plan of Merger with WCI Communities, Inc. (“WCI”), under which the Company will acquire WCI through a merger for a combination of the Company’s Class A common stock and cash. However, the Company has the right to reduce the portion of the merger consideration that will be Class A common stock and increase the portion that will be cash, including the right to make the entire merger consideration cash. The transaction is subject to approval by WCI’s stockholders. It is anticipated that a meeting of WCI stockholders to vote on the transaction will be held in January 2017, and, if the transaction is approved by the WCI stockholders, it will close promptly after the stockholder vote.