CalAtlantic Group, Inc. (NYSE: CAA) on Wednesday after market close announced net income of $167.0 million, or $1.25 per diluted share, for the fourth quarter ended Dec. 31, 2016., compared with net income of $77.5 million, or $0.56 per diluted share in the prior year quarter. Analysts polled by Dow Jones were expecting a profit of $1.09 per share.

The 2016 fourth quarter results include the impact of $2.7 million of merger costs, compared to $44.8 million of merger costs and $64.2 million of purchase accounting adjustments for the 2015 fourth quarter.

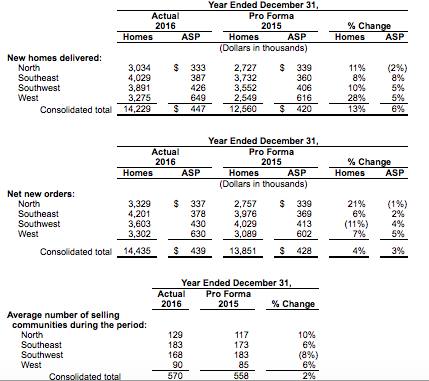

Revenues from home sales for the 2016 fourth quarter increased 18%, to $2.0 billion, as compared to the 2015 fourth quarter, resulting from a 14% increase in new home deliveries and a 3% increase in the average home price to $450,000. The increase in average home price was primarily attributable to product mix and general price increases within select markets.

Net new orders for the 2016 fourth quarter were up 6% from the 2015 fourth quarter, to 2,848 homes, with the dollar value of these orders up 7% to $1.27 billion. The monthly sales absorption rate was 1.64 per community for the 2016 fourth quarter, up 5% compared to the 2015 fourth quarter and down 21% from the 2016 third quarter, consistent with normal seasonal patterns. The cancellation rate for the 2016 fourth quarter was 20%, down compared to 22% for the 2015 fourth quarter and up from 16% for the 2016 third quarter.

The dollar value of homes in backlog increased 4% to $2.7 billion, or 5,817 homes, compared to $2.6 billion, or 5,611 homes, for the 2015 fourth quarter, and decreased 20% compared to $3.3 billion, or 7,307 homes, for the 2016 third quarter. The increase in year-over-year backlog value was driven primarily by the 5% increase in the company’s monthly sales absorption rate. As of December 31, 2016, the average gross margin of the 5,817 total homes in backlog was 20.4%. For the 2,757 homes scheduled to close in the first quarter of 2017, the gross margin in backlog as of such date was 19.5%.

The gross margin from homes sales was 21.8% for the 2016 fourth quarter, negatively impacted by a shift in community mix, a competitive pricing environment, and an increase in direct construction costs per home.

Selling, general and administrative expenses for the 2016 fourth quarter were $191.2 million, or 9.8%, as compared to $171.5 million, or 10.3%, for the 2015 fourth quarter. This 50 basis point improvement was primarily the result of an 18% increase in home sale revenues and the operating leverage associated with the increase in revenue and the synergies gained in connection with the merger with Ryland.

During the 2016 fourth quarter, the company spent $436.0 million on land purchases and development costs, compared to $398.0 million for the 2015 fourth quarter. The company purchased $279.8 million of land, consisting of 3,518 homesites, of which 27% (based on homesites) is located in the North region, 25% in the Southeast region, 21% in the Southwest region, and 27% in the West region. As of December 31, 2016, the company owned or controlled 65,424 homesites, of which 45,699 were owned and actively selling or under development, 14,689 were controlled or under option, and the remaining 5,036 homesites were held for future development or for sale.

CAA ended the quarter with $829.0 million of available liquidity, including $191.1 million of unrestricted home building cash and $637.9 million available to borrow under its $750 million revolving credit facility. The company’s home building debt to book capitalization as of December 31, 2016 and 2015 was 44.8% and 47.5%, respectively, and adjusted net home building debt to adjusted book capitalization was 43.2% and 46.1%, respectively.

During the fourth quarter, the company repurchased 3.0 million shares of its common stock for $95.1 million or an average price of $32.10 per share. For the twelve months ended December 31, 2016 it repurchased 7.3 million shares at an average price of $32.04 and a total spend of $232.5 million.

“In 2016 we delivered double digit top line growth and grew our adjusted pre-tax income by over $145 million<" said Larry Nicholson, president and CEO. "At the same time, we invested approximately $1.6 billion in land acquisition and development, we reduced our net debt-to-cap by 290 basis points and returned over $250 million to shareholders in the form of dividends and share buybacks. We enter 2017 well positioned for continued long-term, profitable growth."