2017’s first public-to-public merger deal, combining two companies of home building’s IPO class of 2013, signals new urgencies, new opportunities, and new challenges for companies whose access to public equity and debt is a financial double-edged sword in today’s home building landscape and housing cycle.

The merger, whose cash is being funded by the much larger Century Communities, adds up to an enterprise value of $1.3 billion, and gives the combined entity an operational footprint in 10 states, 17 markets, and 117 communities. In its purest sense, the deal combines two separate–growing–entities that fit together geographically like a glove. Where Century operates, UCP does not, and the inverse, which means there’s virtually zero overlap in operational resources. The deal allows UCP majority shareholder PICO Holdings to take some cash chips off the table as it, like all other UCP common stock holders, can convert at $5.32 per share. PICO’s ownership in the new combined company would be significantly below 10%.

Per the press statement:

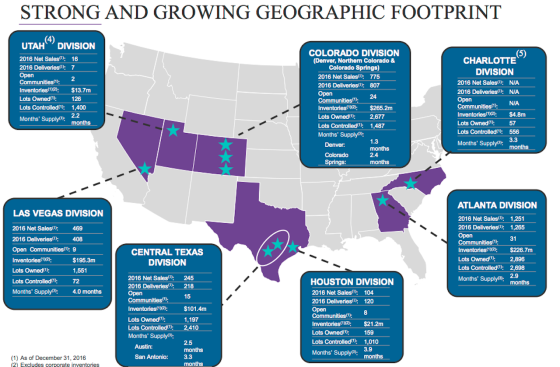

- Increased Scale – The combined company will own or control approximately 25,000 lots and will have a backlog in excess $450 million (calculated on a pro forma basis as of December 31, 2016).

- Geographically Diverse Portfolio with Essentially No Overlap – The combined company portfolio will consist of lots and communities in California, Colorado, Georgia, Nevada, North Carolina, South Carolina, Tennessee, Texas, Utah and Washington. The combination provides for an expanded, national footprint across high-growth markets, which we believe enhances growth prospects while mitigating risks against any potential price and value uncertainties in regional homebuilding markets.

- Seamless Integration and Enhanced Platform – Century and UCP share culturally similar management philosophies and strategic growth objectives which should provide for a unified operating team with extensive land acquisition, entitlement and development expertise.

- Earnings Accretion–The merger is expected to be accretive to the company’s 2018 earnings per share as a result of revenue and cost synergies and economies of scale.

- Increased Market Liquidity – The merger is expected to broaden the combined company’s investor base and increase share liquidity due to the issuance of approximately 4.35 million shares of Century common stock.

For all of these stated gains, questions include:

- Will the entity integrate under the Century Communities name? Will the UCP home building operational brand, Benchmark Communities remain?

- Will the Century executive team, led by brothers Dale and Rob Francescon, cede any of the key strategic management roles to the UCP executive time, or merely consolidate the operations under the Denver-led executive team?

- Now that Century begins to show true scale in the West, Southeast–minus Florida, Texas, Colorado, and the Northwest, will it have the financial clout to continue to be an acquirer of greater local scale and market share in its operating arenas?

- The big question for Century is, is does it now have scale, heft, operating clout, influence with local subcontractors and trades, access to off-market land deals, and above all, top-notch management talent to compete with a smaller, more powerful elite of big builders who command more and more resources in their respective operational spheres?

Since its 2013 IPO, Century has been on an impressive acquisitions run. It started in 2013 with the acquisition of Jimmy Jacobs Homes in the Austin and San Antonio markets, picked up land holdings to establish itself as a major Las Vegas player, bought Houston-based Grand View Builders in August 2014, followed by an Atlanta coup, Peachtree Communities, the market’s #2-ranked builder in November 2014. This past November, Century acquired 50% of Wade Jurney Homes, BUILDER’s fastest-growing private builder for several of the past four or five years.

“We’ve been involved in both companies for several years now, and we introduced them because the cultures, the opportunities for synergies, and the respective opportunities for both make the combination make a lot of sense right now,” said Builder Advisor Group founder and CEO Tony Avila, which provides real estate counsel to Century.

Stepping back from questions pertaining to these two players in particular, the deal signals that institutional investment patience with smaller-scale public players may be finite, suggesting that more of the “mini-me” publics, specifically AV Homes, William Lyon, Green Brick Partners, The New Home Company, and even fast-growing LGI may be ripe for deals amid pressure to consolidate operational and overhead expenses in a slower-growth new home scenario, where behemoths control access to land positions, subcontractors, and buyer pools in any given geographical market.

More to come, but this combination, and more like it, was hinted in a series we recently focused on motivations and drivers of a highly-active mergers and acquisitions environment in home building, here, here, and here.