With the above information in hand, the astute builder can use the work-in-progress report to compute other information that will assist in analyzing jobs in progress. Some information that can be computed from the above data includes:

Projected Gross Profit= Current Contract minus Total Estimated Costs

Current Gross Profit %= Projected Gross Profit divided by Current Contract

Percent Complete= Costs to Date divided by Total Estimated Costs

Revenue Earned= Percent Complete multiplied by Current Contract

Over (Under) Billings= Billed to Date minus Revenue Earned.

The first section of Sample Custom Builders’ work-in-progress report (see Sample Report 2) poses the following questions:

- Why are we behind on billing the Jones job? An under billing on a job in progress can indicate an inaccurate estimate of total costs or a problem with the company’s draw schedule. To best manage cash flow a custom builder should strive to always be in an over-billed situation.

- Why do the margins vary so much between the jobs? Why have the margins changed since the job was originally estimated?

- With the large over billing on the Penn job how will that affect future cash flow?

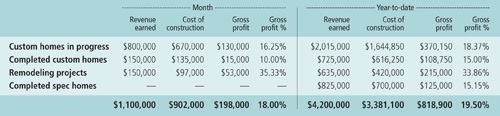

The second section of the work-in-progress report (see Sample Report 3) is helpful in analyzing production. This portion of the report provides the detail behind the custom homes in progress line on the Earnings from Construction schedule. During the month, Sample Custom Builder had $670,000 of construction costs on pre-sold homes run through its system, which was much lower than the company’s monthly budget. The Roberts job was projected to be 25% complete by the end of this period. A perceptive builder will dig further into why the Roberts job is not producing according to plan. Is it due to trades not showing up on the job? Is the superintendent running the job overloaded? Did a trade contractor forget to send in an invoice? Comparing the current month’s margins on a job-by-job basis to the current projected gross profit and the prior month’s projected gross profit percentage, we note that the Jones’ job margins improved during the month and the Johnson job has slipped during the year and particularly during the current month. Margins on the Penn job have also eroded.

This is where the builder who manages and not just watches goes to work investigating the red flags that have been raised by changes in the margins. He digs deeper by asking the three critical questions: What did not go according to plan? Why did things not go according to plan? What can be done so this slide in margins does not continue?

The work-in-progress report is not only a tool to get financial reports on a percentage-of-completion basis or to raise the red flag when a variance from plan exists. This report is also a useful tool in projecting future earnings and cash flow.

Based upon the final section of the work-in-progress report (see Sample Report 4), Sample Custom Builder can project the amount of gross profit that is remaining for custom homes in progress. If there are no further margin adjustments, these four active jobs would produce over $400,000 in gross profit to cover the company’s overhead, which averages about $100,000 per month (four months of overhead coverage). The Penn and Robert jobs will not be completed for 6 and 10 months respectively, so if no new jobs are produced the company will not earn enough margin to cover its overhead. With only $142,500 of cash remaining in these jobs (less than two months of overhead coverage), cash flow is also a future concern. In order to complete the Johnson job, Sample will need to “rob” cash from another job to pay off all of its trades. The big question is: If no new jobs move into production, where will this cash come from? Steve Maltzman, CPA, is president of SMA Consulting in Redlands, Calif. The next article in this series will discuss another critical financial management report: the balance sheet.

For a sample copy of a work-in-progress report, please e-mail smaltzman@smaconsulting.net.