Principal, interest, [property] tax, and insurance.

This set of four financial quantities together form the basis for how mortgage applicants qualify–or not–for a loan to buy a home, and their sum, for those who do qualify, becomes the amount of a monthly mortgage payment.

Now, the center of many builders’ attention, as U.S. lawmakers work on the most massive rewrite of tax code in more than three decades, is on the deductability of mortgage interest payment and the potential evisceration of that tool as a contributing catalyst to homeownership.

While tax reform’s impact on that first “i” in PITI will materially impact fewer geographical markets, fewer buyer types, and fewer builders–think Toll Brothers, New Home Company, Lennar’s newly acquired Standard Pacific-level CalAtlantic Homes, and Ashton Woods, etc., as opposed to lower average-selling-price builders like D.R. Horton, LGI and Century Communities’ Wade Jurney Homes–the Sacred Cow status of the mortage interest deduction commands outsized focus.

Ivy Zelman and her team at Zelman & Associates point out, in the latest edition of The Z Report, that both the House and Senate measures’ biggest sting to individual filers will be among the three out of 10 who itemize deductions on their tax returns (i.e. 70% of tax filers take the Standard Deduction, which would double if either of the two bills pass as is).

Zelman’s analysts level-set the histrionics around debate over the ultimate impact of the two tax bills on people’s sense of “incentive” to become homeowners, using the current levers of tax deductions vs. an enlarged standard deduction. By and large, they assert, the doubled-down standard deduction will put more money in many of the potential first-time buyers’ pockets that many of the builders court with their entry-level communities. The Z Report [which you can sample on a free-trial basis by clicking here] notes:

With permission from Zelman & Associates

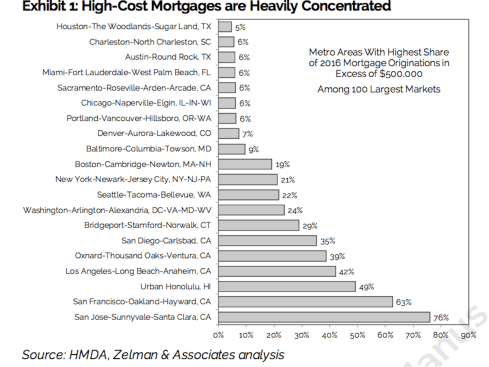

“In 2016, only 7% of unit mortgage originations had a balance higher than $500,000, a figure that has ranged from 3-7% over the last 13 years. These mortgages are heavily concentrated, with just 11 metro areas accounting for 65% of the total, centered in Coastal California, metro New York-New Jersey-Connecticut, metro Washington, D.C. and Honolulu. (See Exhibit 1).

“As with most policy debates, facts take a back seat to rhetoric and various lobbying groups will likely play a significant role in shaping the final bill. Our initial take at this point is that if final tax cuts resemble the two proposals, there will be a period of confusion as households determin the personal impact. However, once the dust settles, we believe that it would be a net cash flow positive for the vast majority of potential homebuyers, which should further support overall home pricing and demand given the tight inventory backdrop.”

That take addresses the switches and levers one might associate with incentives to homeownership. What it does not address is the financial impact of removing the deductability of both state and local taxes and property tax, not to mention one-time capital gains from the sale of a home. This impacts a far greater universe of both potential sellers and buyers as they calculate the pluses and minuses of a transaction, and as they try to qualify for a mortgage using the PITI calculation.

When the “T” is no longer deductible, it changes a potential buyer’s means to make that monthly payment, and creates an entirely new calculus of mortgage loan underwriting.

Doubling the standard deduction might go far to improving many households’ net financial gain, but will that be enough to offset the deductability not only of interest on the mortgage, but property taxes as well as state and local tax?