AS A HOME BUILDER, DO YOU FEEL LIKE PERSONA NON GRATA WITH insurance companies these days? You’re not imagining things. According to insurance experts such as Jenny Schaefer, with Hilb, Rogal and Hobbs, (HRH), an insurance brokerage firm with offices all over the United States, few insurers want to touch a builder with an 8-foot 2×4 these days.

“I think of the 30 major carriers we represent, only three will provide home builders with general liability and workers’ compensation,” Schaefer says. “They’ve just had too many problems. First, it was asbestos, then construction defects and mold. There’s always some new unknown out there.”

If you poke around online, you’ll find a few companies that advertise builders’ insurance. But with most plans, fewer risks are covered than in past years, with a large share of any financial damages falling on the builder’s shoulders.

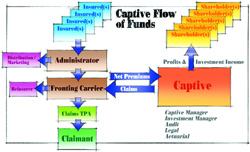

That pattern, says Schaefer, is here to stay. But there is one way builders can temper that bad situation: by enrolling in a “captive” plan. Under this sort of plan, you accept a much larger financial share of any future liability—and pay it in advance. A captive plan often costs much more than conventional insurance used to (when you could get it), but along with the pain come a few perks, including greater control over claims and the potential for profit if the money you have squirreled away is not needed. A captive fund also may be the only way you can secure the additional conventional insurance you need to cover your risk of big losses.

“Builders need to understand that over time they’ll be paying their own claims anyway,” Schaefer explains, “whether that payment is in higher premiums or from a fund they set aside, as in the case of a captive. The difference is, with a captive, they have control over the claims process and who, if anyone, gets paid from that fund.”

Here’s a short primer on the ins and outs of captive insurance—what it is, who provides it, and how it works. If you like the sound of this sort of coverage, be sure to follow our online links to get more information on the topic or to locate a program in your area.

1. Why Go Captive?

Here are a few good reasons to join a captive insurance plan:

2. Option A: Start From Scratch

Creating a captive is much like forming a new business, whether you are a larger builder and want to take that leap or as a small builder interested in banding together with other smaller builders. You also could get a cold shoulder from some existing captives, many of which have strict rules for new members. Here are the bones of the creation process:

3. Option B: Join An Existing Plan

Setting up a captive is complex and fraught with financial and administrative challenges. You may be better off joining an existing captive plan or hiring a third party to set up and run yours. Here are a few reasons why:

4. Benefits Of Control

Several types of captive plans exist, allowing you different levels of control over your capital. In the best-case scenario, you will gain:

5. Caveats: Before You Buy

Be aware of a few “gotchas” before you buy in to a captive insurance plan:

GROUP INSURANCE: A CASE STUDY

| Premium pay-in | $6,000,000 | 100% |

| Fixed expenses | ($2,400,000) | 40% |

| Loss fund for claims | $3,600,000 | 60% |

| Actual claims paid | ($1,800,000) | 30% |

| Underwriting profits | $1,800,000 | 30% |

| Investment income (II) | $481,000 | 8% |

| Total profits and II | $2,281,000 | 38% |

| Premiums: | $6,000,000 | 100% |

| Less profits & II | ($2,281,000) | 32% |

| Ultimate cost of insurance | $3,719,000 | 68% |

The last few years have not been kind to property and casualty (P&C) insurers. Claims have consistently exceeded annual premiums. Many firms have reserves with which they make up these deficits—but some have gone under. The survivors have restructured, raised premiums, and tightened policies to try to check losses. Where home builders are concerned, they point to class-action lawsuits over mold and asbestos contamination. In addition, workers’ compensation claims continue to pummel insurers. For example, a Syracuse, N.Y., carpenter recently walked away with $1,100,000 after he fell 20 feet on a jobsite and fractured his wrist. Other big payouts to homeowners followed hurricanes, winter storms, and flooding. And the 2003 claims for wildfire losses may beat all previous records.