Hovnanian Enterprises (NYSE:HOV) on Thursday morning reported net income of $22.3 million, or $0.14 per common share, for the fourth quarter of fiscal 2016 ended Oct. 31, compared with $25.5 million, or $0.17 per common share, in the fourth quarter of the previous year. For the fiscal year ended October 31, 2016, the company reported a net loss of $2.8 million, or $0.02 per common share, compared with a net loss of $16.1 million, or $0.11 per common share, in all of fiscal 2015.

Analysts were expecting a gain of $0.13 per share for the quarter and a loss of $0.01 for the fiscal year.

For the fourth quarter of fiscal 2016, Adjusted EBITDA increased 13.6% to $96.4 million compared with $84.9 million during the fourth quarter of 2015. For all of fiscal 2016, Adjusted EBITDA increased 53.5% to $231.2 million compared with $150.6 million during all of fiscal 2015.

Consolidated net contracts per active selling community increased 11.4% to 7.8 net contracts per active selling community for the fourth quarter of fiscal 2016 compared with 7.0 net contracts per active selling community in the fourth quarter of fiscal 2015. Net contracts per active selling community, including unconsolidated joint ventures, increased 4.2% to 7.4 net contracts per active selling community for the quarter ended October 31, 2016 compared with 7.1 net contracts, including unconsolidated joint ventures, per active selling community in the fourth quarter of fiscal 2015.

Consolidated active selling communities decreased 23.7% from 219 communities at the end of the prior year’s fourth quarter to 167 communities as of October 31, 2016, which was impacted by the sale of ten communities in Minneapolis and Raleigh and the conversion of four consolidated communities into unconsolidated joint venture communities. As of the end of the fourth quarter of fiscal 2016, active selling communities, including unconsolidated joint ventures, decreased 17.9% to 188 communities compared with 229 communities at October 31, 2015.

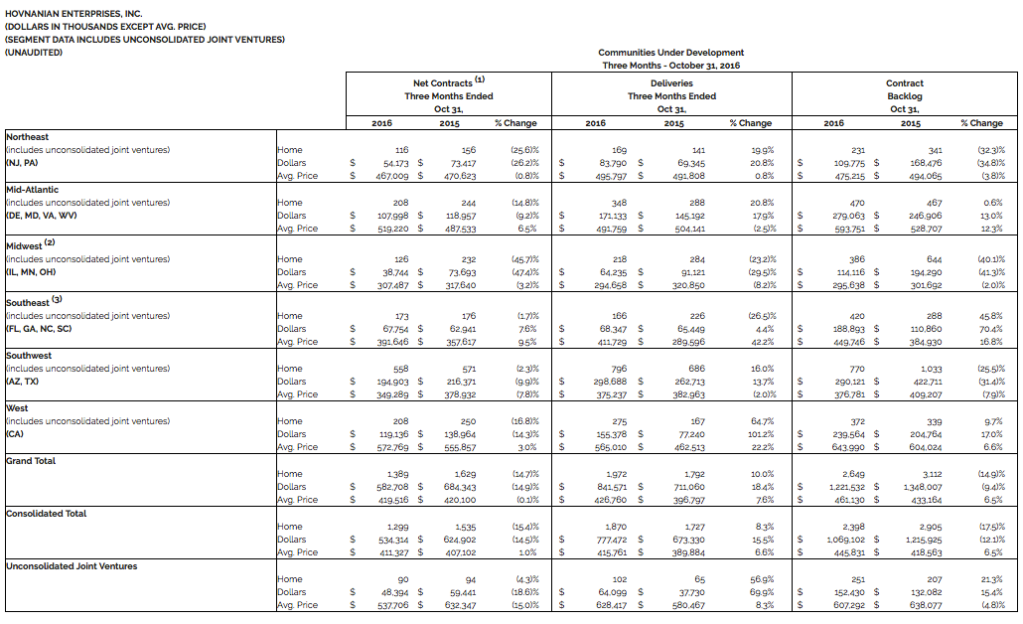

The dollar value of consolidated net contracts decreased 14.5% to $534.3 million for the three months ended October 31, 2016 compared with $624.9 million during the same quarter a year ago. The dollar value of net contracts, including unconsolidated joint ventures, during the fourth quarter of fiscal 2016 decreased 14.9% to $582.7 million compared with $684.3 million in last year’s fourth quarter.

The dollar value of consolidated net contracts increased 2.6% to $2.51 billion for all of fiscal 2016 compared with $2.45 billion in the previous fiscal year. The dollar value of net contracts, including unconsolidated joint ventures, for the twelve months ended October 31, 2016 increased 0.9% to $2.67 billion compared with $2.65 billion in fiscal 2015.

The number of consolidated net contracts, during the fourth quarter of fiscal 2016, decreased 15.4% to 1,299 homes compared with 1,535 homes in the prior year’s fourth quarter. In the fourth quarter of fiscal 2016, the number of net contracts, including unconsolidated joint ventures, decreased 14.7% to 1,389 homes from 1,629 homes during the fourth quarter of fiscal 2015.

The number of consolidated net contracts, during the twelve-month period ended October 31, 2016, decreased 1.2% to 6,109 homes compared with 6,183 homes in the same period of the previous year. During all of fiscal 2016, the number of net contracts, including unconsolidated joint ventures, was 6,380 homes, a decrease of 2.6% from 6,547 homes during fiscal 2015.

As of October 31, 2016, the dollar value of contract backlog, including unconsolidated joint ventures, was $1.22 billion, a decrease of 9.4% compared with $1.35 billion as of October 31, 2015. The dollar value of consolidated contract backlog, as of October 31, 2016, decreased 12.1% to $1.07 billion compared with $1.22 billion as of October 31, 2015.

As of October 31, 2016, the number of homes in contract backlog, including unconsolidated joint ventures, decreased 14.9% to 2,649 homes compared with 3,112 homes as of October 31, 2015. The number of homes in consolidated contract backlog, as of October 31, 2016, decreased 17.5% to 2,398 homes compared with 2,905 homes as of the end of the fourth quarter of fiscal 2015.

Consolidated deliveries were 1,870 homes in the fourth quarter of fiscal 2016, an 8.3% increase compared with 1,727 homes in the fourth quarter of fiscal 2015. For the three months ended October 31, 2016, deliveries, including unconsolidated joint ventures, increased 10.0% to 1,972 homes compared with 1,792 homes in the fourth quarter of the prior year.

Consolidated deliveries were 6,464 homes for all of fiscal 2016, a 17.4% increase compared with 5,507 homes in the same period of fiscal 2015. For the twelve months ended October 31, 2016, deliveries, including unconsolidated joint ventures, increased 16.2% to 6,712 homes compared with 5,776 homes in the twelve months of the prior fiscal year.

The contract cancellation rate, including unconsolidated joint ventures, for the fourth quarter of fiscal 2016 was 21%, compared with 20% in the fourth quarter of fiscal 2015.

The valuation allowance was $627.9 million as of October 31, 2016. The valuation allowance is a non-cash reserve against the tax assets for GAAP purposes. For tax purposes, the tax deductions associated with the tax assets may be carried forward for 20 years from the date the deductions were incurred.

After paying off $320.0 million of debt that matured in October 2015, January 2016 and May 2016, total liquidity at the end of the fourth quarter of fiscal 2016 was $346.6 million.

During the fourth quarter of fiscal 2016, land and land development spending was $131.4 million compared with $192.1 million in last year’s fourth quarter. For the year ended October 31, 2016, land and land development spending was $567.0 million compared to $656.5 million in the prior fiscal year.

As of October 31, 2016, the land position, including unconsolidated joint ventures, was 31,281 lots, consisting of 14,165 lots under option and 17,116 owned lots, compared with a total of 37,659 lots as of October 31, 2015.

During the fourth quarter of fiscal 2016, approximately 2,100 lots, including unconsolidated joint ventures, were put under option or acquired in 37 communities.

“For fiscal 2016, we grew revenues by 28%, reduced our SG&A ratio by 250 basis points, paid off $260 million of public debt at maturity and returned to profitability. Nonetheless, fiscal 2016 was a very challenging year,” stated Ara K. Hovnanian, chairman and CEO. “The debt markets remained closed to companies with our credit ratings and we needed to raise funds to pay off $260 million of maturing public debt. This led to our decision to enhance our liquidity by increasing our use of land bank financings and joint ventures, as well as exiting four underperforming markets. This adversely affected our ability to invest as aggressively in new land parcels as previously planned. However, we ended the year with a liquidity position of $347 million, allowing us to once again actively seek land investment opportunities, which should ultimately result in community count growth and, assuming no change in market conditions, higher levels of profitability in the future,” concluded Hovnanian.