The New Home Company Inc. (NYSE: NWHM), ALISO VIEJO, Calif., on Wednesday reported a profit of $13.8 million, or $0.66 per diluted share, for the fourth quarter ended Dec. 31, up 13% from $12.2 million, or $0.69 per diluted share in the prior-year quarter. The most recent analyst consensus from Dow Jones, taken three months ago, was for a gain of $0.70 per share.

The results included $3.5 million of pretax inventory impairments, or $0.10 per diluted share after tax.

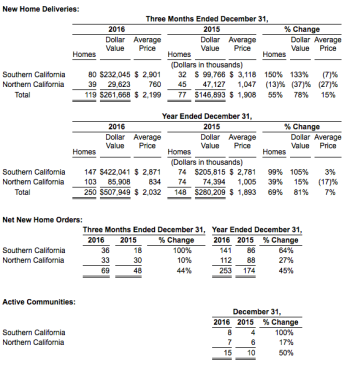

Total revenue was up 66% to $322.4 million as home sales revenue rose 78% to $261.7 million. The increase in home sales revenue was driven primarily by a 55% increase in deliveries and a 15% increase in the average selling price of homes to $2.2 million. The increase in average selling price was due to a 150% increase in deliveries from Southern California operations, which had a significantly higher average selling price than the company’s Northern California operations due to the high concentration of luxury product.

Gross margin from homes sales was 14.4% and included $2.4 million in inventory impairments related to two active home-building communities. Excluding inventory impairments, gross margin from home sales for the 2016 fourth quarter was 15.3%* versus 16.6%* in the prior year period. The decline in home sales gross margin before impairments as compared to the prior year was due primarily to a change in mix, including lower margins in master-plan communities located in Irvine, and to a lesser extent, lower margins in the Bay Area. These decreases were partially offset by higher margins from the initial deliveries in the company’s Crystal Cove communities in Newport Coast, Ca. Adjusted gross margin from home sales for the 2016 fourth quarter, which excludes interest in cost of home sales and inventory impairments, was 16.2% compared to 17.7%.

SG&A as a percentage of home sales revenue was 7.9% versus 9.1% in the prior year period. The 120 basis point improvement in the SG&A rate was largely attributable to a 78% increase in home sales revenue, which was driven by a significant increase in new home deliveries and higher average selling prices due to a heavier Southern California mix.

Net new home orders were up 44% to 69 homes, compared to 48 homes in the prior year period. The company’s monthly sales absorption pace was consistent with the prior period at 1.6 sales per average selling community. Average selling communities were up 50% from the prior year, ending the year with 15 communities compared to 10 as of the end of the prior year.

The dollar value of the company’s wholly owned backlog at the end of the 2016 fourth quarter was up 12% year-over-year to $187.3 million and totaled 79 homes, compared to $166.6 million and 67 homes in the prior year period. The increase in backlog dollar value primarily related to the increase in net new home orders.

Fee building revenue for the 2016 fourth quarter increased 27% to $60.8 million primarily due to an increase in fee building construction activity. Fee building gross margin was $2.7 million, or 4.5%, compared to $4.1 million, or 8.5%, in the prior year period. The reduction in fee building gross margin percentage was largely due to a decrease in management fees received from joint ventures, which were $2.0 million during the 2016 fourth quarter compared to $4.1 million in the prior year period. The decrease in management fees from JVs was primarily the result of fewer deliveries and lower home sales revenue from JV communities, which is consistent with the company’s strategic shift to emphasize wholly owned operations.

The company’s share of joint venture income for the 2016 fourth quarter was $3.3 million, compared to $4.6 million in the prior year period. The decrease in joint venture income was driven by a 47% reduction in JV home sales revenues, resulting from a 32% decrease in the JV average selling price and a 22% decrease in JV home deliveries.

Total revenue of the JVs was $86.7 million and net income was $9.8 million, compared to $155.1 million and $25.9 million in the prior year period, respectively. Home sales revenue of the JVs was $72.0 million, compared to $135.2 million in the prior year period.

At the end of the 2016 fourth quarter, the JVs had nine active selling communities, up from eight at the end of the prior year period. Net new home orders from JVs for the 2016 fourth quarter increased 55% to 48 homes as compared to 31 homes in the prior year period which was driven by a doubling of the JV sales absorption rate from 1.0 sales per month per community in the 2015 fourth quarter to 2.0 per month in the 2016 fourth quarter. The dollar value of homes in backlog from unconsolidated JVs at the end of the 2016 fourth quarter was $55.4 million from 62 homes, compared to $117.9 million from 109 homes in the prior year period.

“While we expect 2017 to be a transition year for our company as we diversify our product portfolio with new communities at lower price points, our commitment to being the category leader in each of our product niches remains the same,” said Larry Webb, New Home CEO. “We continue to identify attractive opportunities in California and other markets, and we are poised to take advantage of these opportunities and create long-term value for our shareholders.”