Toll Brothers, Inc., Horsham, Pa. (NYSE:TOL) on Wednesday reported net income of $70.4 million, or $0.42 per share, for its first fiscal quarter ended Jan. 31, compared to net income of $73.2 million and $0.40 per share diluted in FY 2016’s first quarter. Analysts were anticipating a gain of $0.34 per share.

The results included pre-tax inventory write-downs totaling $4.7 million, compared to $1.3 million in FY 2016’s first quarter.

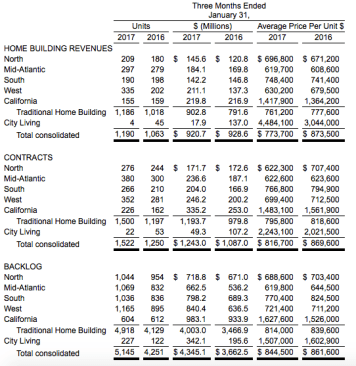

Revenues of $920.7 million and home building deliveries of 1,190 units were approximately flat in dollars and increased 12% in units, compared to FY 2016’s first-quarter total of $928.6 million and 1,063 units. The average price of homes delivered declined to $773,700, due to changes in product mix, compared to $873,500 in FY 2016’s first quarter.

Net signed contracts of $1.24 billion and 1,522 units rose 14% in dollars and 22% in units, compared to FY 2016’s first quarter totals of $1.09 billion and 1,250 units. The average price of net signed contracts was $816,700, compared to $869,600 in FY 2016’s first quarter. The company said the decline was due in part to the acquisition of Boise-based Coleman Homes, a decline in the number of contracts signed in the City Living division compared to one year ago and an increase in townhome contracts in the North and Mid-Atlantic regions.

On a per-community basis, FY 2017’s first-quarter net signed contracts was 4.73 units per community, compared to first quarter totals of 4.34 in FY 2016, 4.09 in FY 2015, 3.95 in FY 2014, and 4.34 in FY 2013.

For the first three weeks of FY 2017’s second quarter, beginning February 1, 2017, non-binding reservations deposits were up 16% in units, compared to the same period in FY 2016.

Backlog of $4.35 billion and 5,145 units rose 19% in dollars and 21% in units, compared to FY 2016’s first-quarter-end backlog of $3.66 billion and 4,251 units. The average price of homes in backlog was $844,500, compared to $861,600 at FY 2016’s first-quarter end.

Gross margin, as a percentage of revenues, was 20.4% in FY 2017’s first quarter, compared to 23.3% in FY 2016’s first quarter. Adjusted Gross Margin, which excludes interest and inventory write-downs, was 23.9%, compared to 26.9% in FY 2016’s first quarter.

Other income and Income from unconsolidated entities totaled $59.1 million, compared to $22.4 million in FY 2016’s first quarter.

The company ended its first quarter with 321 selling communities, compared to 310 at FYE 2016, and 291 at FY 2016’s first-quarter end.

On February 21, 2017, the company announced that its board approved the initiation of a cash dividend to shareholders. The first quarterly dividend of $0.08 per share, equivalent to approximately 1% annualized of the Company’s current share price, will be paid on April 28, 2017 to shareholders of record on the close of business on April 14, 2017.

During the first quarter of FY 2017, the Company repurchased approximately 557,000 shares of its common stock at an average price of $27.33, for a total purchase price of $15.2 million.

Toll increased the mid-point of its delivery guidance for full FY 2017 by 100 units and now expects FY 2017 deliveries of between 6,700 and 7,500 units with an average price of between $775,000 and $825,000 and projects second-quarter deliveries of between 1,350 and 1,650 units with an average price of between $810,000 and $835,000. The company expects its second-quarter FY 2017 Adjusted Gross Margin to be between 23.8% and 24.2% of revenues.

FY 2017 second-quarter SG&A is expected to be approximately 11.4% of second quarter revenues.

Douglas C. Yearley, Jr., Toll Brothers’ chief executive officer, stated: “FY 2017’s first-quarter contracts rose 14% in dollars and 22% in units compared to the first quarter of FY 2016. This was our tenth consecutive quarter of year-over-year growth in contract dollars and units, with double digit increases in each of the past three quarters. And for the first 3 weeks of FY 2017’s second quarter, non-binding reservation deposits were up 16% in units, compared to the same period in FY 2016.

“FY 2017 should be another year of substantial growth. Deliveries are projected to increase from 6,100 in FY 2016 to between 6,700 and 7,500 in FY 2017. We should continue to post strong gross margins. And Other income and Income from Joint Ventures (Unconsolidated entities) is projected to increase from $100 million in FY 2016 to between $160 million and $200 million in FY 2017. This should produce significantly higher earnings per share in FY 2017 versus FY 2016 and improve our ROE to 12% of beginning equity.

“As the only national home building company focused on the highly fragmented luxury market, we continue to enjoy strong demand and produce industry-leading contract growth,” said Douglas C. Yearley, Jr., Toll CEO. Our strategic plan to diversify geographically and by product type enables us to appeal to a wide demographic interested in a luxury home…Our ‘affordable luxury’ product lines reach a large and growing base of affluent move-up, empty-nester and millennial buyers. Our strong balance sheet gives us a financial edge over the small and mid-sized builders who are our primary competition in the luxury market.

“Contracts in our City Living division, which operates primarily in the urban metro New York City market, were down year-over-year this quarter, while our quarter-end backlog was up, our gross margins continue to far exceed Company averages and we continue to have confidence in the quality of our locations,” Yearley continued. “In conjunction with our geographic and product diversification, we are also developing a significant portfolio of luxury rental properties, most of which will be built and owned in joint ventures. In total, our portfolio includes in excess of 10,000 units built, in construction or planned across the nation.”

“Last night we announced that we will begin paying a quarterly dividend equal to $.08 per share, or approximately 1% annualized of our current share price. This dividend is the next step in the maturation of our company and, along with our stock repurchases, reflects our commitment to return cash to our shareholders and improve our return on equity. This dividend should not in any way restrict our opportunities to invest in future growth, either through land acquisitions, company acquisitions or other strategic initiatives. We also believe a dividend at this time and at this level will broaden our investor base.”

Robert I. Toll, executive chairman, stated: “The housing market continues on its path of steady growth. Total housing starts rose in 2016 to approximately 1.2 million units, the highest level since 2007. However, despite this increase, nationwide housing starts remain well below historic norms of 1.6 million annually, even as population has continued to grow over the past decade. With home price appreciation strengthening personal balance sheets, the Dow Jones Industrial Average surpassing 20,000 for the first time, and low unemployment, we believe the housing outlook for 2017 remains favorable.

“The pent-up demand of the past seven years may be starting to release, bringing more buyers into the market, especially in the move-up segment, where rising home values are giving buyers more equity when they sell their homes in order to move up,” said Robert I. Toll, executive chairman. “The leading edge of the millennial generation has begun to form families, have children and buy homes. And maturing baby boomers continue to demonstrate strong demand for our Active Adult homes. With supplies of new and existing homes still tight, we believe a rise in demand could push home prices higher.”