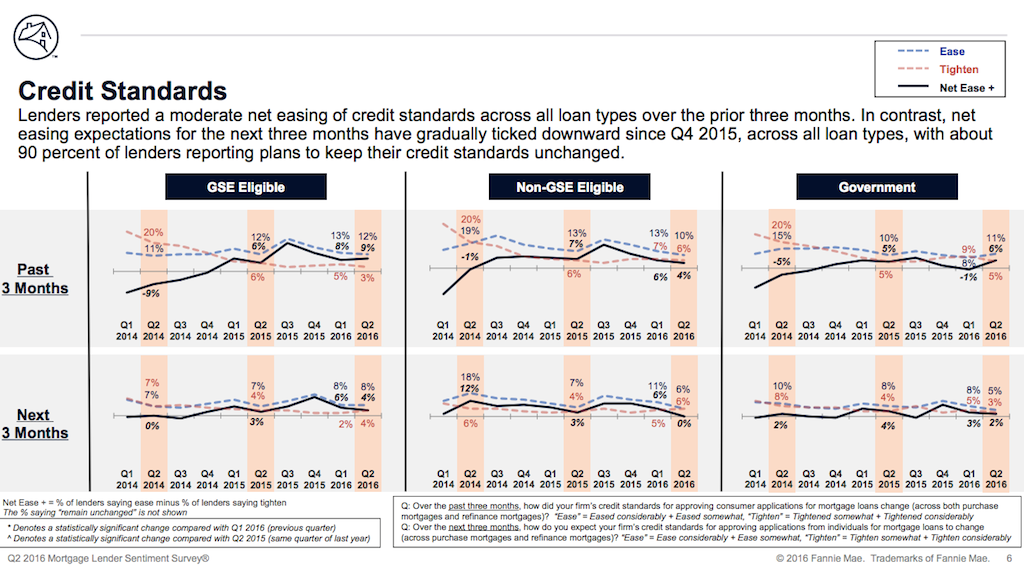

Here’s data that suggests 9 out of 10 lenders think the credit box is open wide enough, thank you very much.

Fannie Mae’s second quarter Mortgage Lender Sentiment Survey has good news, on the one hand, that consumer demand for purchase mortgages just about equals year-ago levels of home loan demand. On the other hand, plans to ease credit standards further have all but evaporated, as 90% of lenders report that they’ll stand pat.

There are smart industry experts who believe the credit box is now opened wide enough; that qualification terms and standards are where they need to be, and that getting approved for a mortgage is easier these days than many people think.

What do you think?

After all, the Fannie data highlights that while consumer demand may be where it’s supposed to be, lender supply is reluctant to go there. The reason being, fear–under new bank regulations–of having to take back loans that may go bad if a borrower defaults.

It’s why, per a National Association of Home Builders analysis, banks–large and small–make up just 4 in 10 home purchase mortgage loans these days–down from half in 2010, in the pre-Dodd Frank era. Banks’ ability to profit off making mortgage loans is very different, and harder in the post-Dodd Frank era, so fewer of them are doing it, and they’re doing it less.

This is part of a vicious circle in housing: overly tight credit; regulatory-cost laden new homes that price out of reach of many would-be buyers; suppressed housing starts, all of whose impact spreads into broader economies.

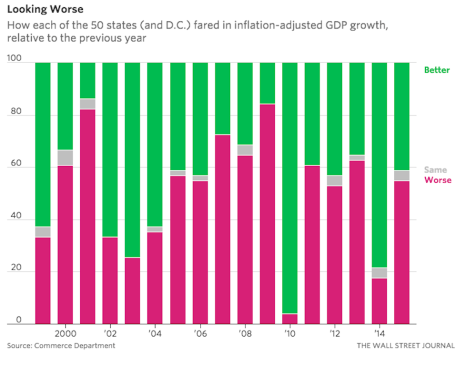

Here, Wall Street Journal reporter Jeffrey Sparshott spotlights, on Federal Reserve Open Market Committee-eve, a report that more than half of the United States experienced an economic decline vs. the prior year on a state by state basis.

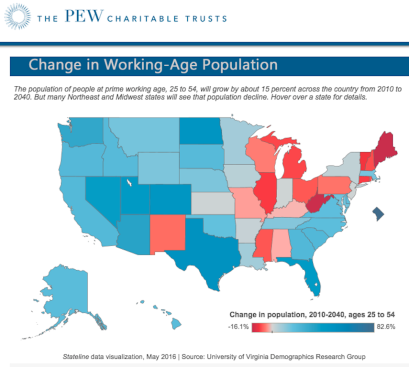

And here, Pew Charitable Trusts shows evidence that the outlook among some states’ economies is further diminishing returns based on a loss of workforce participants. The linkage between housing development and construction, housing attainability, and economic growth gets more and more conspicuous in its absence.

When housing functions as it should in the economy, it serves three primary benefits in the broader economy: it provides people with shelter; it creates jobs; and it creates outsized consumer demand among the households who buy the new homes, feeding local economies, and corporate profitability.

The snail’s pace recovery in housing that began to take shape in 2012 and 2013 with the mass-scale absorption of distressed residential real estate, and took further shape with the high-end and discretionary buyer wave in 2014 and 2015, is still awaiting the all-important activation of the lower-price tier, move-out-of-rental buyer universe–housing’s mezzanine level.

This is why the Fannie report on lender sentiment, which points toward little or no progress in making an overly constricted credit box more inclusive, is a discouraging signal right now.