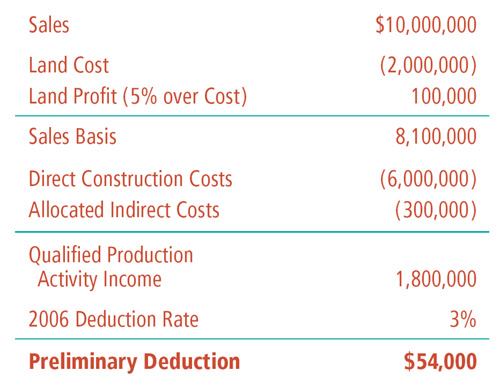

For asset acquisitions don’t forget Section 179, which allows a deduction of up to $108,000 of fixed asset purchases in 2006. Passenger vehicles used in the business are not allowable for the section 179 deduction, and it is limited to $25,000 for purchases of heavy SUVs (defined as having a gross vehicle weight between 6,001 and 14,000 pounds).

Employee Benefits

There is a wide range of retirement plans that allow you to save some of your wages not subject to income tax. Some plans even provide for a tax deduction for the company. Following is a brief introduction to some of the programs. Be careful of discriminatory retirement and deferred compensation plans as well as limitations that may be placed on owners and highly compensated employees.

- A SIMPLE plan provides for up to $10,000 of earnings to be set aside in a retirement plan not being subject to taxes until they are distributed. The company can also contribute to this plan and get a tax deduction.

- For 2006, up to $15,000 can be contributed to a company 401(k) plan with an additional $5,000 for employees over 50. Ask your tax advisor about safe harbor rules, which can remove the contribution limit of owners and highly compensated employees, as well as about employing your spouse to obtain additional family tax deferrals.

- Profit-sharing plans can be established that provide for company contributions (and deductions) that may be tiered, providing a larger contribution for key employees.

- There are a number of medical benefit plans, including a flexible spending account (FSA), cafeteria plan, health savings account (HSA), and health reimbursement arrangements (HRA), that enable you to pay medical, dependent care, and other expenses with pretax dollars. The spent dollars reduce taxable earnings and escape federal, state, local, and Social Security taxes. Be careful of exclusions for stockholders and highly compensated employees of an S Corp, LLC, or other flow-through entity.

Improve Your Financial Statements

For builders who are required to present financial statements to their bank or outside investor there are a number of things you may want to do prior to year-end to improve the look of the statements. When making some year-end transactions you need to look at both the tax and financial statement effects. Sometimes transactions that would improve your financial statement may actually increase your current-year tax liability.

- Consider selling off noncurrent assets and turning them into current assets. This move would improve your working capital ratio, which your bank looks at as a measure of liquidity.

- Another method of improving liquidity is to refinance your debt, moving it from current (due by the end of 2007) to long term. As an owner of a C Corporation you may want to issue a long-term note to the company and use the proceeds to pay off current debt.

- Minimize prepaid expenses. Often bankers throw out prepaid expenses in their calculation of working capital.

The year end is also a good time to make sure that all of your corporate activities are up to date. The main advantage of having a corporation is to protect your personal liability. However, lawyers have been able to “pierce the corporate veil” when the entity was not properly treated as a corporation. Be sure to:

- update your corporate minutes so they document all activities mentioned in your bylaws that need to be acted upon by the corporation’s officers.

- make sure that all related party transactions are properly documented. Officer loans to and from the corporation need to be formalized. Check with your tax advisor on interest requirements.

One last thing: It’s also time to start looking forward to 2007. If you haven’t already started, now is a good time to work on your business plan and operating budgets for next fiscal year. And so the cycle of planning, budgeting, and reviewing begins again.